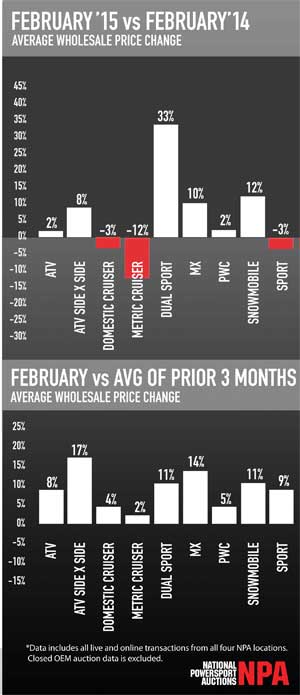

Average Wholesale Pricing (AWP) in February showed signs of strength with all major categories rising over the prior three month average.

Average Wholesale Pricing (AWP) in February showed signs of strength with all major categories rising over the prior three month average.

We are seeing a rise in bidder attendance as well, but values remain softer than expected for this time of year, especially metric cruisers. While more dealers are reporting additional need for inventory than last month, many remain sufficiently stocked due to the prolonged winter weather.

In February domestic cruiser AWP rose like we have come to expect around this time of the year, but remains below last year’s levels. Metric cruisers (especially large displacement), on the other hand, remained flat and significantly below last year’s average pricing.

Sport bikes are trending up slightly, similar to prior years, while all off-road categories have gotten off to a better start than compared to the same time last year. From a product mix perspective, the ratio of domestic cruisers and other street bikes remained roughly constant in February, and the percentage of ATVs declined.

In comparison to book value, the wholesale price to clean NADA book ratio is trending five points lower than last year for all categories, with metric cruisers tracking almost 10 points behind prior years.

Repo volumes are trailing forecasts, which is a sign of continued consumer credit strength and the need for more financing options.

Some selling dealers have delayed liquidating inventory or are setting unrealistic reserve prices in anticipation of a bigger price jump in the coming spring months, slightly reducing dealer consignment volumes and sale conversion rates.

However, based upon current trends, we expect the spring rise to be notably less significant than last year.