Average Wholesale Pricing in April was up over the prior three months, especially for off-road product categories.

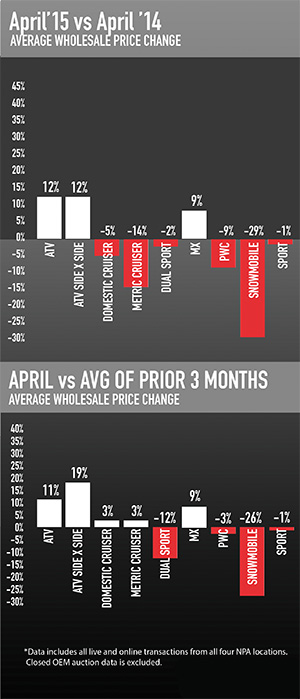

[dropcap]O[/dropcap]ff-road product pricing in April was above last year’s level, which is partly a function of demand outpacing limited supply as well as a more expensive product mix. The most notable price gain over the prior month was for Side-by-Sides (SxS), which appears to be the result of a more expensive product mix, slightly younger model ages and dealer demand.

Overall, the spring peak this year continues to be softer than years past, with slower rises in domestic and metric cruisers. All street motorcycles continue to pace below last year’s pricing, despite dealers stating they need more products to meet their needs. Metric cruisers continue to be uncharacteristically flat for the season, which appears to be almost entirely product mix – the average metric cruiser sold in April is more than a year older and in slightly less condition than the prior year’s average.

Compared to NADA book values, wholesale pricing in April followed more typical seasonal behavior, suggesting that book values are accurately reflecting slightly softer market conditions this year. MSRP of units sold grew in April, which indicates a slightly more expensive product mix despite the older average model age. The MSRP for any specific model year is generally up for 2014 models going through the auction, with domestic cruiser and SxS MSRP up notably, and lower MSRP for 2014 sport and metric models than prior years.

The ratio of domestic cruisers sold increased in April while the ratio of ATVs declined. The mix of other street product volumes sold remained constant. Wholesale volumes sold remained below last year’s levels and down slightly from last month. This is a function of continued low repo default rates and powersports dealers holding on to their trades and retail inventory longer than last year. Dealers continue to report robust used retail sales as consumers seek out mid-price product and pre-owned retail financing continues to improve.

We anticipate the spring wholesale seasons to stretch into June this year. Pricing will begin to taper as normal, but more gradually than last year. With new pre-owned financing programs on the horizon, as well as smarter trade valuations by dealers, the potential exists for a busier summer and fall market as well.

All data provided by National Powersport Auctions. For more information, please visit www.npauctions.com or call (888) 292-5339.